2026 Capital Gains Tax: Navigating New Investment Adjustments

Understanding the 2026 Capital Gains Tax Adjustments and How They Affect Your Investments (RECENT UPDATES)

The financial world is constantly evolving, and with each passing year, new regulations and adjustments can significantly impact how individuals and businesses manage their wealth. As we look towards 2026, a crucial area of focus for investors and financial planners alike is the anticipated adjustments to capital gains tax. These changes, often introduced to address economic shifts, fiscal policy objectives, or societal needs, can have far-reaching implications for investment strategies, retirement planning, and overall financial health. Understanding the intricacies of the 2026 Capital Gains Tax adjustments is not just about compliance; it’s about strategic planning and optimizing your financial future.

Capital gains tax is levied on the profit realized from the sale of a non-inventory asset that was purchased at a lower price. This includes assets like stocks, bonds, real estate, and even collectibles. The rate at which these gains are taxed can vary significantly based on several factors, including the type of asset, the length of time it was held (short-term vs. long-term), and the taxpayer’s overall income level. The upcoming adjustments in 2026 could introduce new rate structures, alter holding period definitions, or implement new thresholds that trigger different tax treatments. For many, these changes could mean a substantial difference in their after-tax investment returns.

This comprehensive guide aims to demystify the recent updates and potential implications of the 2026 Capital Gains Tax adjustments. We will delve into what these changes might entail, explore their potential impact on various investment types, and, most importantly, provide actionable strategies to help you navigate this evolving tax landscape. Whether you are a seasoned investor, a budding entrepreneur, or simply someone looking to understand how these tax changes might affect your personal finances, this article will serve as your go-to resource for informed decision-making.

The Foundations of Capital Gains Tax: A Brief Overview

Before we dive into the specifics of the 2026 Capital Gains Tax adjustments, it’s essential to have a solid understanding of the current capital gains tax framework. This foundational knowledge will help contextualize the upcoming changes and highlight why they are so significant. Capital gains are generally categorized into two main types: short-term and long-term.

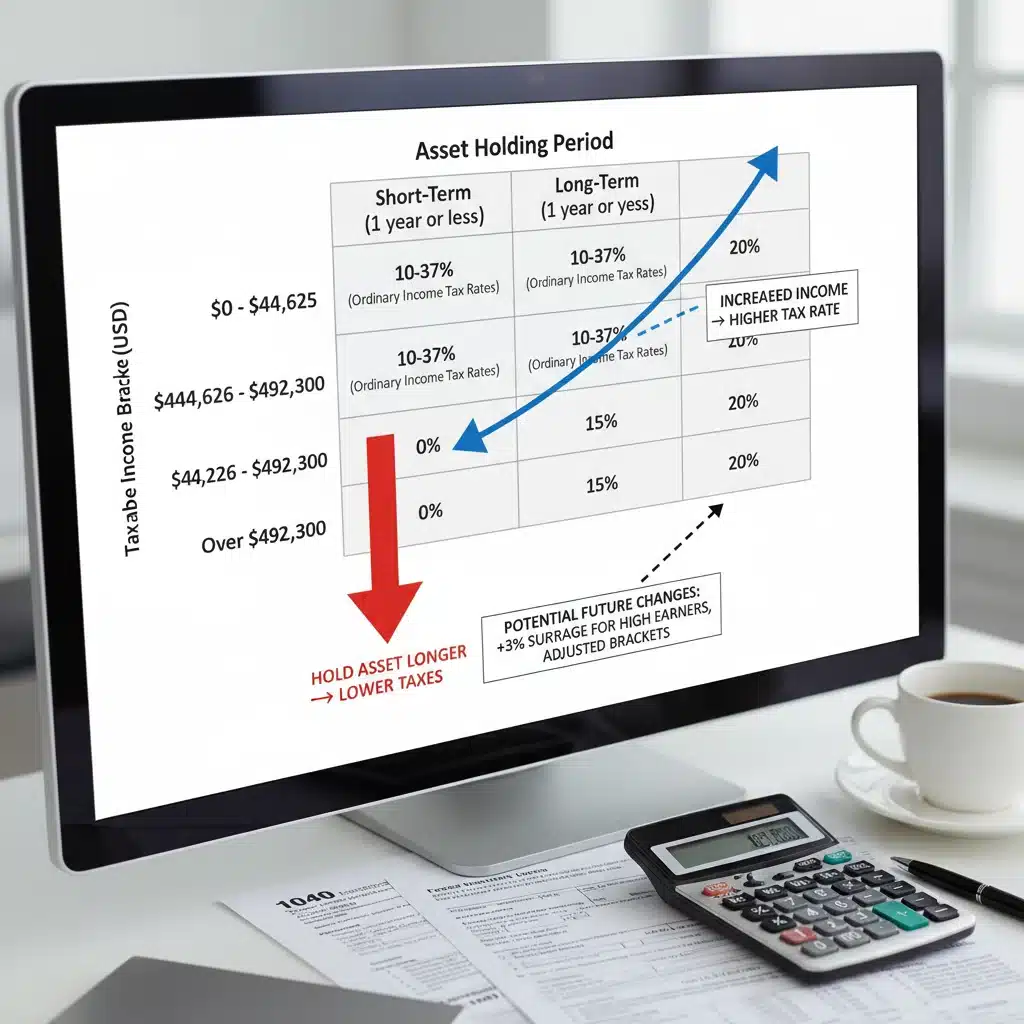

- Short-Term Capital Gains: These are profits from the sale of assets held for one year or less. They are typically taxed at your ordinary income tax rates, which can be as high as 37% for the highest earners.

- Long-Term Capital Gains: These are profits from the sale of assets held for more than one year. Historically, long-term capital gains have enjoyed more favorable tax treatment, with rates typically set at 0%, 15%, or 20%, depending on your taxable income.

The distinction between short-term and long-term is critical, as it often dictates the tax burden. The rationale behind taxing long-term gains at lower rates is often to encourage long-term investment, which is seen as beneficial for economic growth and stability. However, this distinction, along with the specific rates and income thresholds, is precisely what can be subject to change with new legislation.

Key Factors Influencing Capital Gains Tax Rates

Several factors can influence the capital gains tax rates you pay:

- Taxable Income: Your overall income level plays a significant role in determining your capital gains tax rate, especially for long-term gains. As your income rises, so does the likelihood of falling into higher capital gains tax brackets.

- Filing Status: Your filing status (single, married filing jointly, head of household, etc.) also affects the income thresholds for different tax rates.

- Type of Asset: While most assets fall under the general capital gains rules, certain assets, like collectibles (e.g., art, antiques, coins), may be subject to different, often higher, long-term capital gains rates (up to 28%). Real estate gains can also be subject to specific rules, such as depreciation recapture.

- Location: State and local capital gains taxes can also apply, adding another layer of complexity to the overall tax burden. These vary significantly by jurisdiction and are often independent of federal changes.

Understanding these fundamental aspects of capital gains tax is the first step towards effectively preparing for the adjustments anticipated in 2026. These changes could potentially redefine these categories, alter the rates, or introduce new tax provisions that impact how your investment gains are calculated and taxed.

Anticipated 2026 Capital Gains Tax Adjustments: What’s on the Horizon?

While specific legislative details are often subject to ongoing debate and political processes, economic indicators, policy proposals, and historical trends provide strong clues about the likely direction of 2026 Capital Gains Tax adjustments. Several key areas are typically considered when governments look to modify capital gains taxation.

Potential Changes to Long-Term Capital Gains Rates

One of the most significant areas of potential adjustment involves the long-term capital gains rates. There has been ongoing discussion in policy circles regarding increasing these rates, particularly for high-income earners. The arguments often center on issues of wealth inequality and the need for increased government revenue. Possible scenarios include:

- Alignment with Ordinary Income Rates: A more radical proposal sometimes discussed is aligning long-term capital gains tax rates more closely with ordinary income tax rates for certain high-income brackets. While a full alignment is often met with strong opposition due to concerns about disincentivizing investment, a partial alignment or an increase in the top long-term capital gains rate is a more plausible adjustment.

- New Income Thresholds: It’s also possible that the income thresholds for the existing 0%, 15%, and 20% long-term capital gains rates could be adjusted, either by lowering them to bring more income into higher tax brackets or by introducing new, higher brackets for ultra-high-net-worth individuals.

- Surtaxes: The introduction of additional surtaxes on capital gains for very high incomes is another mechanism that could be employed to increase revenue without fundamentally altering the rate structure for most investors.

Changes to Holding Periods and Definitions

Another area ripe for adjustment is the definition of what constitutes a ‘long-term’ asset. The current one-year holding period is relatively short compared to some other developed nations. Lengthening this holding period, for example, to two or three years, could significantly impact short-term trading strategies and encourage even longer-term investment. Such a change would reclassify many currently ‘long-term’ gains as ‘short-term,’ subjecting them to higher ordinary income tax rates.

Impact on Specific Asset Classes

The 2026 Capital Gains Tax adjustments may also include specific provisions for certain asset classes:

- Real Estate: Changes to depreciation recapture rules or adjustments to the Section 121 exclusion (for primary home sales) could be on the table. While unlikely to completely remove the primary home exclusion, modifications to its thresholds or frequency could affect homeowners.

- Collectibles and Other Unique Assets: The current 28% maximum rate for collectibles might be revisited, or the definition of what constitutes a ‘collectible’ could be broadened, bringing more assets under this higher tax umbrella.

- Digital Assets (Cryptocurrencies): As the digital asset market matures, governments are increasingly looking at how to tax these assets more effectively. While often treated as property for tax purposes, specific guidance or adjustments related to cryptocurrency capital gains could emerge, especially concerning staking, mining, or DeFi activities.

Estate Tax and Step-Up in Basis

While not strictly capital gains tax, the ‘step-up in basis’ rule is closely related and frequently discussed in conjunction with capital gains. This rule allows inherited assets to be revalued at their market price on the date of the owner’s death, effectively eliminating capital gains tax on appreciation that occurred during the deceased’s lifetime. Proposals to modify or eliminate the step-up in basis, especially for large estates, could significantly increase the capital gains tax liability for heirs upon the sale of inherited assets. This is a highly contentious issue, but its potential impact is immense for estate planning.

It is crucial to remember that these are potential adjustments based on current discussions and historical patterns. Investors should stay informed through reliable financial news sources and consult with tax professionals as legislative proposals solidify. Proactive planning based on anticipated changes is key to mitigating adverse effects.

Impact on Investment Strategies: Navigating the New Landscape

The potential 2026 Capital Gains Tax adjustments will undoubtedly require investors to re-evaluate and potentially modify their investment strategies. What worked effectively under previous tax regimes may no longer be optimal. Here’s how various aspects of your investment approach might be affected and what you can do to adapt.

Re-evaluating Asset Allocation

If long-term capital gains rates increase, especially for higher income brackets, investors might become more conscious of the tax efficiency of their portfolios. This could lead to a shift in asset allocation:

- Growth vs. Income Assets: Assets that generate significant capital appreciation (growth stocks, certain real estate) might become less attractive if their gains are taxed at higher rates. Conversely, income-generating assets (dividend stocks, bonds) might see increased interest, though their tax treatment (ordinary income) would still need to be considered.

- Tax-Advantaged Accounts: The appeal of tax-advantaged accounts like 401(k)s, IRAs (Traditional and Roth), and 529 plans for education savings will likely grow. These accounts allow investments to grow tax-deferred or tax-free, shielding gains from annual taxation and potentially from future higher capital gains rates. Maximizing contributions to these accounts should be a top priority.

- Tax-Loss Harvesting: This strategy, which involves selling investments at a loss to offset capital gains and potentially a limited amount of ordinary income, will become even more valuable. Investors may become more diligent in identifying opportunities for tax-loss harvesting throughout the year.

Adjusting Holding Periods

Should the definition of a ‘long-term’ asset be extended beyond one year, investors would need to adapt their holding periods. This could discourage frequent trading and encourage a more buy-and-hold approach to ensure favorable long-term capital gains treatment. Active traders, in particular, would need to reassess their strategies, as more of their profits could be classified as short-term gains, subject to higher ordinary income tax rates.

Considerations for Real Estate Investors

Real estate investors could face unique challenges and opportunities:

- Depreciation Recapture: If depreciation recapture rules are tightened or rates increased, it could impact the net proceeds from selling appreciated properties.

- 1031 Exchanges: Like-kind exchanges (1031 exchanges) allow investors to defer capital gains tax on the sale of investment property if they reinvest the proceeds into a similar property. The utility of 1031 exchanges may increase if capital gains rates rise, making tax deferral even more attractive. However, these rules are also periodically reviewed, so their continued availability and scope should be monitored.

- Opportunity Zones: Investments in Qualified Opportunity Funds (QOFs) offer significant tax benefits, including deferral of capital gains and potential tax-free growth if held for a sufficient period. These could become even more appealing under a higher capital gains tax regime.

Estate Planning Implications

Changes to the step-up in basis rule would have profound implications for estate planning. If the step-up is limited or eliminated, heirs would inherit assets with the original cost basis, meaning they would be responsible for capital gains tax on all appreciation when the asset is eventually sold. This would necessitate a re-evaluation of how assets are passed down and could lead to increased use of trusts or other estate planning tools to minimize future tax liabilities.

The Role of Diversification

Diversification remains a cornerstone of sound investment strategy, but its tax implications could become even more significant. Spreading investments across various asset classes, industries, and geographies can help mitigate risk, and now, potentially, tax exposure. Including tax-efficient investments, such as municipal bonds (which are often federally tax-exempt and sometimes state and local tax-exempt), might become more attractive for high-income earners.

Strategic Tax Planning for the 2026 Capital Gains Tax Landscape

Proactive and informed tax planning is paramount to successfully navigating the impending 2026 Capital Gains Tax adjustments. Waiting until the last minute can lead to missed opportunities and unnecessary tax burdens. Here are several strategies to consider implementing now.

Maximize Tax-Advantaged Accounts

As mentioned earlier, tax-advantaged accounts are your first line of defense against higher capital gains taxes. Maximize contributions to:

- 401(k)s and IRAs: These retirement accounts allow your investments to grow tax-deferred. Traditional accounts offer an upfront tax deduction, while Roth accounts provide tax-free withdrawals in retirement. For those anticipating higher income in retirement, Roth conversions might be a strategy to consider, especially if current tax rates are lower than future anticipated rates.

- Health Savings Accounts (HSAs): Often referred to as a ‘triple tax advantage’ account, contributions are tax-deductible, investments grow tax-free, and withdrawals for qualified medical expenses are tax-free. HSAs can be an excellent long-term investment vehicle for those with high-deductible health plans.

- 529 Plans: For education savings, 529 plans offer tax-free growth and withdrawals for qualified educational expenses.

Effective Use of Tax-Loss Harvesting

Tax-loss harvesting involves selling investments at a loss to offset capital gains. If your capital gains rates are increasing, the value of offsetting those gains becomes even greater. You can offset an unlimited amount of capital gains and up to $3,000 of ordinary income annually. Any excess losses can be carried forward to future years. Regular portfolio reviews can help identify opportunities for tax-loss harvesting throughout the year, not just at year-end.

Consider Gifting Appreciated Assets

Gifting appreciated assets to individuals in lower tax brackets (e.g., children or grandchildren) can be an effective strategy if they intend to sell the assets. The recipient would pay capital gains tax at their lower rate, potentially saving the family money overall. However, be mindful of gift tax rules and annual exclusion limits. For larger gifts, consult with a financial advisor to understand the implications.

Charitable Giving Strategies

For philanthropically inclined investors, donating appreciated assets directly to a qualified charity can be a highly tax-efficient strategy. If you donate stock or mutual fund shares held for more than one year, you generally don’t have to pay capital gains tax on the appreciation, and you can deduct the fair market value of the donation (up to certain limits). This can be more advantageous than selling the asset, paying the capital gains tax, and then donating the cash.

Rebalancing and Portfolio Adjustments

As the 2026 Capital Gains Tax changes approach, it might be prudent to rebalance your portfolio to align with your risk tolerance and new tax considerations. This could involve selling off positions with significant embedded gains while rates are still favorable, or strategically shifting towards investments that are more tax-efficient under the new regime. However, any rebalancing should be done carefully, considering transaction costs and potential short-term capital gains if assets are sold too quickly.

Consult with Tax and Financial Professionals

The most crucial strategy is to engage with qualified tax advisors and financial planners. They can provide personalized advice based on your specific financial situation, investment goals, and risk tolerance. They can help you:

- Understand the precise implications of the 2026 changes for your portfolio.

- Develop a customized tax-efficient investment strategy.

- Identify specific opportunities for tax savings.

- Stay updated on legislative developments and adjust your plans accordingly.

Tax laws are complex and constantly changing. A professional can help you navigate these complexities and ensure you are taking advantage of all available strategies to minimize your tax liability.

Long-Term Outlook and Economic Implications of the 2026 Capital Gains Tax

The adjustments to the 2026 Capital Gains Tax are not just about individual tax bills; they also carry broader economic implications that can shape market behavior, investment trends, and national fiscal policy. Understanding this wider context can help investors anticipate secondary effects and make more informed decisions.

Market Volatility and Investor Behavior

Any significant change in capital gains taxation can introduce a period of market uncertainty. Investors might react by accelerating or delaying asset sales, leading to increased volatility. For example, if higher rates are anticipated, some investors might try to realize gains before the new rates take effect, potentially causing a temporary surge in selling activity. Conversely, if lower rates are expected (though less likely in the current climate for capital gains), investors might hold onto assets, expecting to sell them more favorably later.

Changes in tax policy can also influence investor psychology. A perception of less favorable tax treatment for investments could, in theory, reduce overall market participation or shift capital towards less tax-sensitive investments or international markets, although the extent of this effect is often debated.

Impact on Entrepreneurship and Venture Capital

Capital gains tax rates are particularly relevant for entrepreneurship and venture capital. The ability of founders and early investors to realize significant tax-efficient gains is a powerful incentive for innovation and risk-taking. If long-term capital gains rates increase substantially, it could potentially dampen the enthusiasm for starting new businesses or investing in high-growth, early-stage companies, as the ultimate reward becomes less attractive after tax. Policymakers often weigh this against the desire for increased revenue, creating a delicate balance.

Government Revenue and Fiscal Policy

A primary driver for adjusting capital gains tax rates is often the government’s need for revenue. Increased capital gains tax collections can fund public projects, reduce national debt, or support other fiscal policy objectives. However, the exact impact on revenue is complex, as higher rates can sometimes lead to less realized gains if investors choose to hold assets longer or find other tax-efficient strategies. The ‘Laffer Curve’ concept, which suggests there’s an optimal tax rate beyond which revenue might decline, is often cited in these debates.

International Competitiveness

Countries often compare their tax policies, including capital gains rates, to remain competitive. If a nation’s capital gains taxes become significantly higher than those of other major economies, it could potentially lead to capital flight or discourage foreign investment. This is a factor policymakers consider to ensure that tax changes do not inadvertently harm the country’s economic standing on the global stage.

Wealth Distribution and Economic Equity

Discussions around capital gains tax frequently intersect with issues of wealth distribution and economic equity. Proponents of higher capital gains taxes often argue that it’s a way to ensure that wealthier individuals, who disproportionately benefit from capital appreciation, contribute more to public finances. Opponents, however, contend that it penalizes successful investment and can stifle economic growth. The 2026 Capital Gains Tax adjustments will inevitably be part of this ongoing societal and economic dialogue.

Preparing for the Future: Actionable Steps for Investors

Given the potential for significant changes with the 2026 Capital Gains Tax adjustments, taking proactive steps now is more important than ever. Here’s a summary of actionable steps you can implement to prepare your portfolio and financial plan.

1. Review Your Current Investment Portfolio

Conduct a thorough review of your investment portfolio. Understand the cost basis of your assets, identify positions with significant unrealized gains, and assess your current asset allocation. This baseline understanding is crucial for strategic planning.

2. Understand Your Tax Bracket

Know your current marginal income tax bracket and how it relates to capital gains tax rates. This will help you anticipate how potential rate changes might specifically affect you.

3. Maximize Contributions to Tax-Advantaged Accounts

Prioritize contributing the maximum allowable amounts to your 401(k), IRA, HSA, and 529 plans. These accounts offer significant tax benefits that become even more valuable in a potentially higher tax environment.

4. Explore Tax-Loss Harvesting Opportunities

Regularly monitor your portfolio for opportunities to harvest tax losses. This can be done throughout the year, not just at year-end, to offset capital gains and reduce your taxable income.

5. Consider Strategic Realization of Gains

If you anticipate significantly higher capital gains rates in 2026, you might consider strategically realizing some gains in 2024 or 2025 while current, potentially more favorable, rates apply. This decision should be made in consultation with a financial advisor, considering your overall financial picture and long-term goals.

6. Re-evaluate Estate Plan

If changes to the step-up in basis rule are a strong possibility, review your estate plan with an attorney. Strategies involving trusts or other gifting mechanisms might become more critical to mitigate future tax liabilities for your heirs.

7. Stay Informed and Adaptable

Legislative processes can be dynamic. Stay updated on political developments, proposed legislation, and economic forecasts from reputable sources. Be prepared to adapt your strategies as more concrete details about the 2026 Capital Gains Tax adjustments emerge.

8. Seek Professional Financial and Tax Advice

This cannot be stressed enough. Tax laws are complex, and their impact is highly individualized. A qualified financial advisor and tax professional can provide tailored guidance, help you understand the nuances of the upcoming changes, and develop a robust, tax-efficient strategy that aligns with your personal circumstances and financial objectives.

Conclusion

The prospect of 2026 Capital Gains Tax adjustments presents both challenges and opportunities for investors. While the specifics are still unfolding, a proactive and informed approach is the best defense against potential adverse impacts and the best offense for optimizing your financial outcomes. By understanding the fundamentals of capital gains tax, anticipating potential changes, and implementing strategic planning techniques, you can navigate the evolving tax landscape with confidence. Remember, successful investing isn’t just about choosing the right assets; it’s also about managing them in the most tax-efficient way possible. Start planning today to secure your financial future against the backdrop of these important tax reforms.

and IRA Limits")

Limits & Roth IRA Benefits")

Contribution Limits 2026: Maximize Your Retirement Savings")