2026 Federal Reserve Interest Rate Hikes: Investment Portfolio Strategies

Navigating the 2026 Federal Reserve Interest Rate Hikes: Strategies for Your Investment Portfolio (RECENT UPDATES)

The financial world is perpetually in motion, and few events cast a longer shadow than anticipated shifts in monetary policy. As we look towards 2026, the prospect of Federal Reserve interest rate hikes is a topic of paramount importance for investors worldwide. Understanding the potential implications of these hikes and developing robust strategies to navigate them is not merely advisable but essential for safeguarding and growing your investment portfolio. This comprehensive guide aims to dissect the forecasted 2026 Fed Rates, explore their multifaceted impact, and provide actionable strategies to help you position your investments for success.

The Federal Reserve, often referred to as ‘the Fed,’ plays a pivotal role in the U.S. economy through its monetary policy decisions. Its primary mandates are to foster maximum employment and maintain price stability. Interest rate adjustments are among its most potent tools to achieve these goals. When inflation pressures build, or the economy appears to be overheating, the Fed typically raises interest rates to cool down economic activity. Conversely, during economic downturns, it lowers rates to stimulate growth. The anticipated 2026 Fed Rates adjustments are expected to be a response to the evolving economic landscape post-pandemic, characterized by persistent inflationary pressures and a robust labor market.

Forecasting the exact timing and magnitude of future rate hikes is inherently challenging, as the Fed’s decisions are data-dependent and subject to change. However, market analysts and economists continuously monitor key indicators – including inflation data, employment figures, GDP growth, and global economic trends – to project the Fed’s likely path. By 2026, many anticipate that the Fed will have continued its trajectory of normalizing interest rates, bringing them closer to historical averages, or even slightly above, depending on the inflation outlook. This normalization process, while a sign of a healthy economy, can introduce volatility and reprice assets across various markets. Therefore, a proactive approach to your investment strategy is critical.

Understanding the Rationale Behind Expected 2026 Fed Rates Hikes

To effectively prepare for the impact of rising 2026 Fed Rates, it’s crucial to understand the underlying economic conditions that would prompt such actions. The primary driver for interest rate increases is often the need to combat inflation. After periods of extensive quantitative easing and fiscal stimulus, economies can experience elevated inflation. The Fed’s response is to raise the federal funds rate, which influences other interest rates throughout the economy, making borrowing more expensive and thereby dampening demand. This, in theory, helps to bring inflation back down to the Fed’s target of around 2%.

Another significant factor is a strong labor market. When unemployment rates are low and wages are rising rapidly, it can also contribute to inflationary pressures. A tight labor market gives the Fed more leeway to raise rates without fear of significantly derailing economic growth or employment. By 2026, if the labor market remains robust and wage growth continues, it further supports the case for higher interest rates. The global economic environment also plays a role. Geopolitical events, supply chain disruptions, and the economic performance of major trading partners can all influence the Fed’s decisions. For instance, global inflationary pressures can spill over into the U.S. economy, necessitating a stronger domestic monetary policy response.

Furthermore, the Fed’s communication strategy, often referred to as ‘forward guidance,’ is a key component of its policy toolkit. By signaling its intentions well in advance, the Fed aims to manage market expectations and reduce volatility. Investors should pay close attention to the minutes of Federal Open Market Committee (FOMC) meetings, speeches by Fed officials, and economic projections to glean insights into the likely path of 2026 Fed Rates. These communications provide valuable clues about the Fed’s assessment of the economy and its future policy direction, allowing investors to anticipate potential shifts and adjust their portfolios accordingly.

Impact of Rising 2026 Fed Rates on Different Asset Classes

The ripple effects of rising interest rates are far-reaching, impacting virtually every asset class. Understanding these impacts is the first step in formulating an effective investment strategy for 2026 Fed Rates.

Bonds and Fixed Income

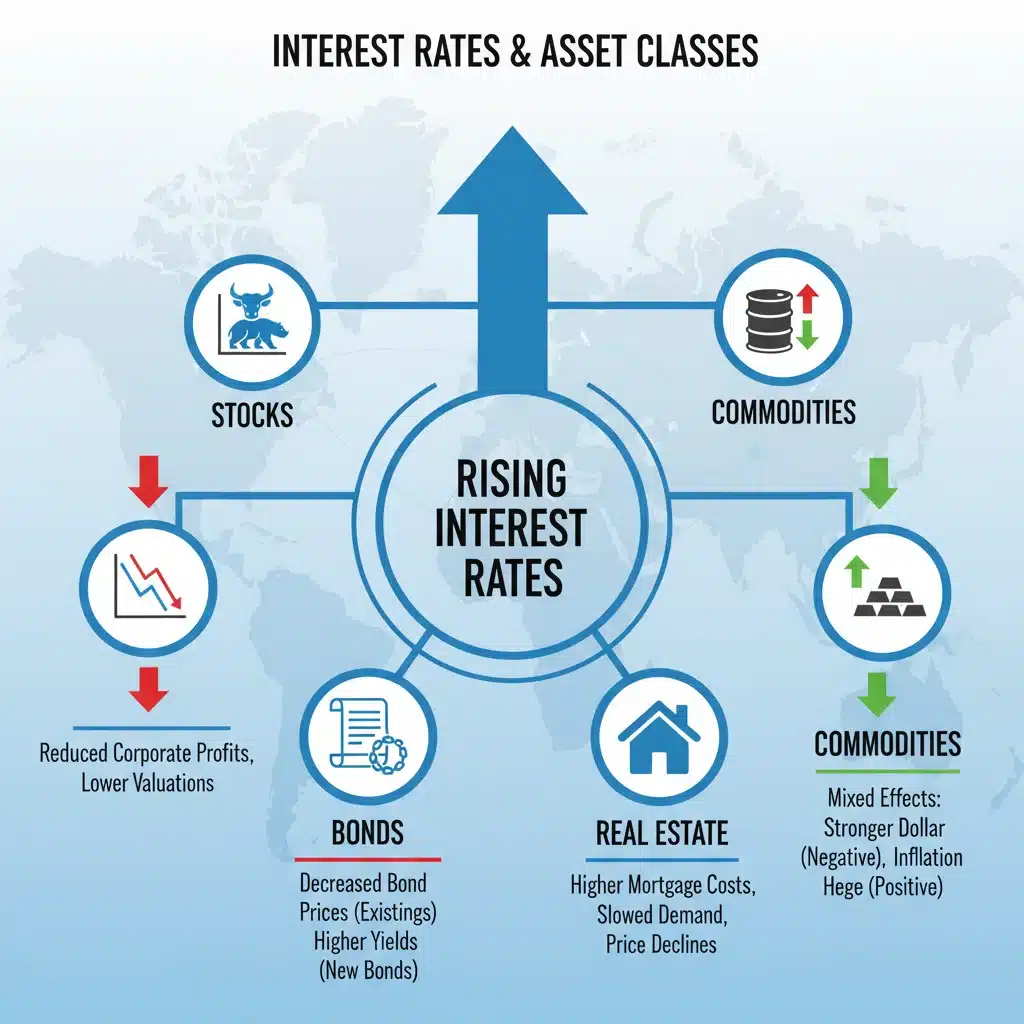

Perhaps the most direct impact of rising interest rates is felt in the bond market. When new bonds are issued with higher yields, existing bonds with lower yields become less attractive, causing their prices to fall. This inverse relationship means that bondholders can experience capital losses in a rising rate environment. Longer-duration bonds are typically more sensitive to interest rate changes than shorter-duration bonds. Investors holding long-term government bonds or corporate bonds may see their principal values decline. However, for those looking to invest in fixed income, higher rates mean new bond issues will offer more attractive yields, providing an opportunity for increased income over time. Diversifying across different maturities and considering floating-rate bonds or inflation-protected securities (TIPS) can be prudent strategies.

Equities (Stocks)

The impact on the stock market is more nuanced. Higher interest rates increase borrowing costs for companies, which can reduce corporate profits. This is particularly true for highly leveraged companies or those in capital-intensive industries. Additionally, higher rates make it more expensive for consumers to borrow, potentially dampening consumer spending and, consequently, corporate revenues. Growth stocks, especially those in the technology sector, are often more sensitive to rising rates because their valuations are heavily reliant on future earnings, which are discounted at a higher rate. Value stocks, which tend to have more stable earnings and pay dividends, may be more resilient. Sectors that can pass on increased costs to consumers, such as utilities and consumer staples, or those that benefit from higher rates, like banks and financial institutions, might perform relatively better. Therefore, a shift towards value-oriented stocks and sectors with strong pricing power could be beneficial in a rising 2026 Fed Rates environment.

Real Estate

Rising interest rates typically lead to higher mortgage rates, which can cool down the housing market by making homeownership less affordable. This can impact real estate prices and demand. Commercial real estate can also be affected as financing costs increase for developers and investors. However, certain segments of the real estate market, such as those with stable rental income streams or properties located in high-growth areas, might be more insulated. REITs, which often pay high dividends, can be sensitive to interest rate changes, as their yields compete with bond yields. Investors should assess their real estate holdings for interest rate sensitivity and consider diversification into different property types or geographic regions.

Commodities

The relationship between interest rates and commodities is complex. A stronger U.S. dollar, often a consequence of rising interest rates, can make dollar-denominated commodities like oil and gold more expensive for foreign buyers, potentially dampening demand and prices. However, if rising rates are a response to persistent inflation, some commodities, particularly precious metals like gold, can act as an inflation hedge, maintaining their value when the purchasing power of fiat currencies declines. Industrial commodities, on the other hand, are more closely tied to global economic growth, which could be slowed by higher rates. Diversification into a basket of commodities can help mitigate risks associated with specific commodity price fluctuations.

Strategies for Your Investment Portfolio in a Rising 2026 Fed Rates Environment

Proactive planning is key to navigating the challenges and opportunities presented by rising 2026 Fed Rates. Here are several strategies to consider for your investment portfolio:

1. Reassess Your Asset Allocation

Review your current asset allocation to ensure it aligns with your risk tolerance and financial goals in a rising rate environment. You might consider reducing exposure to long-duration bonds and growth stocks that are highly sensitive to interest rates. Conversely, increasing allocation to shorter-duration bonds, dividend-paying stocks, and sectors that tend to perform well during periods of rising rates could be beneficial. Diversification across different asset classes, geographies, and investment styles remains a cornerstone of sound portfolio management.

2. Focus on Quality and Value

In a rising rate environment, companies with strong balance sheets, consistent cash flows, and robust pricing power tend to outperform. These ‘quality’ companies are better equipped to absorb higher borrowing costs and maintain profitability. Value stocks, which are often overlooked and trade below their intrinsic value, may also offer a compelling investment opportunity. As the cost of capital rises, the market may become more discerning, favoring companies with proven profitability over speculative growth stories. Look for businesses that can thrive even if economic growth moderates due to higher rates.

3. Consider Inflation-Protected Securities (TIPS)

If the Fed is raising rates to combat inflation, then inflation-protected securities (TIPS) can be an attractive option. The principal value of TIPS adjusts with inflation, as measured by the Consumer Price Index (CPI), providing a hedge against the erosion of purchasing power. While their yields might still be affected by rising nominal rates, the inflation adjustment component offers a level of protection that traditional bonds do not.

4. Explore Floating-Rate Instruments

Floating-rate bonds and loans have interest payments that adjust periodically based on a benchmark interest rate, such as LIBOR or SOFR. This means that as interest rates rise, the income generated by these instruments also increases, making them less susceptible to the capital losses experienced by fixed-rate bonds in a rising rate environment. They can be a valuable addition to the fixed-income portion of your portfolio.

5. Evaluate Real Estate Exposure

For real estate investors, consider properties with stable cash flows and strong tenant demand. Diversifying beyond residential real estate into commercial sectors like industrial or specialized properties (e.g., data centers, self-storage) might offer more resilience. REITs specializing in these sectors could also be an option. Additionally, consider the debt structure of any real estate investments; fixed-rate mortgages will be more favorable than variable-rate loans if rates are expected to climb.

6. Financial Sector Opportunities

Banks and other financial institutions often benefit from rising interest rates. As rates increase, the spread between what banks pay on deposits and what they earn on loans typically widens, leading to higher net interest margins and improved profitability. Investing in well-managed financial institutions with strong balance sheets could be a strategic move in anticipation of higher 2026 Fed Rates.

7. Review Debt Management

For individuals and businesses, rising interest rates mean higher costs for variable-rate debt. If you have significant variable-rate loans (e.g., credit cards, adjustable-rate mortgages), consider consolidating or refinancing them into fixed-rate options if possible, to lock in lower rates before further hikes. Reducing overall debt can also improve your financial resilience during periods of higher borrowing costs.

8. Maintain Liquidity

Having a portion of your portfolio in highly liquid assets, such as cash or short-term high-yield savings accounts, can provide flexibility. This liquidity allows you to capitalize on investment opportunities that may arise from market volatility caused by rate hikes, or to cover unexpected expenses without having to sell investments at unfavorable prices. While cash returns may lag inflation, having a strategic reserve is always prudent.

9. Consider Alternative Investments

Certain alternative investments, such as private equity, hedge funds, or infrastructure projects, may offer diversification benefits and less correlation with traditional markets. However, these investments often come with higher fees, illiquidity, and require a higher level of due diligence. They are typically more suitable for sophisticated investors with a significant risk appetite and long-term horizon.

Recent Updates and Future Outlook for 2026 Fed Rates

The Federal Reserve’s stance is dynamic, constantly adapting to new economic data and global developments. Recent updates from FOMC meetings and economic projections indicate a continued commitment to bringing inflation under control, even if it means maintaining a restrictive monetary policy for an extended period. While the pace of rate hikes might slow down as inflation shows signs of easing, the general trajectory towards higher rates by 2026 remains a strong possibility.

Key indicators to watch include the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) price index, which is the Fed’s preferred measure of inflation. Employment reports, including non-farm payrolls and wage growth, will also be critical. Any significant shifts in global economic growth or geopolitical stability could also influence the Fed’s decisions. For instance, a global recession could prompt the Fed to re-evaluate its tightening path, while persistent supply-side shocks could necessitate more aggressive action.

Analysts are also closely watching the ‘dot plot,’ which illustrates FOMC members’ projections for the federal funds rate. While not a definitive forecast, it provides valuable insight into the collective thinking of the committee. The evolution of the dot plot over successive meetings can signal whether the Fed is becoming more hawkish or dovish in its outlook for 2026 Fed Rates.

The Importance of Professional Guidance

Navigating the complexities of a rising interest rate environment, especially when anticipating significant shifts in 2026 Fed Rates, can be challenging for even seasoned investors. Economic forecasts are subject to change, and market reactions can be unpredictable. This is where the expertise of a qualified financial advisor becomes invaluable.

A financial advisor can help you:

- Assess Your Individual Situation: They can evaluate your specific financial goals, risk tolerance, and current portfolio to tailor strategies that are best suited for you.

- Develop a Customized Plan: Based on the anticipated impact of rising rates, an advisor can help you construct a diversified portfolio designed to mitigate risks and capitalize on opportunities.

- Stay Informed: Advisors continuously monitor economic data, Fed communications, and market trends, providing timely insights and helping you make informed decisions.

- Manage Emotions: During periods of market volatility, it’s easy to make impulsive decisions driven by fear or greed. A professional advisor can provide an objective perspective and help you stick to your long-term plan.

- Rebalance Your Portfolio: As market conditions change, periodic rebalancing is crucial to maintain your desired asset allocation. An advisor can guide you through this process.

While this article provides general strategies, personalized advice is crucial. The impact of 2026 Fed Rates will vary depending on your specific investment horizon, income needs, and existing financial commitments. Therefore, consulting with a financial professional can provide the tailored guidance you need to confidently navigate the evolving economic landscape.

Conclusion: Preparing for 2026 Fed Rates with Confidence

The prospect of Federal Reserve interest rate hikes in 2026 is a significant consideration for every investor. While it presents potential challenges, it also creates opportunities for those who are well-prepared and strategic. By understanding the rationale behind the Fed’s actions, anticipating the impact on various asset classes, and implementing proactive investment strategies, you can position your portfolio for resilience and growth.

Key takeaways include reassessing asset allocation, prioritizing quality and value, considering inflation-protected and floating-rate instruments, and strategically managing real estate and debt. Staying informed about recent Fed updates and economic indicators is crucial, as is seeking professional financial guidance to tailor strategies to your unique circumstances. The financial markets are dynamic, but with careful planning and a disciplined approach, you can navigate the anticipated 2026 Fed Rates environment with confidence, ensuring your investment portfolio is robust and aligned with your long-term financial aspirations.

Remember, the goal is not to predict the future with perfect accuracy, but to build a portfolio that is adaptable and resilient to a range of economic scenarios. By taking these steps now, you can transform potential headwinds into tailwinds, securing your financial future in the face of evolving monetary policy.