Maximize Social Security Benefits 2026: Unlock $500 More

Unlock Up to $500 More: Insider Strategies for Maximizing Social Security Benefits in 2026

Are you looking ahead to retirement and wondering how to make the most of your Social Security? The year 2026 might seem a ways off, but strategic planning now can significantly impact your future financial security. For many, Social Security represents a crucial component of their retirement income, and understanding how to Maximize Social Security 2026 benefits could mean an extra $500 or more per month. This isn’t just about waiting to claim; it’s about a multi-faceted approach that considers various factors, from your claiming age to spousal benefits and the ever-important Cost-of-Living Adjustment (COLA).

The landscape of Social Security is constantly evolving, with annual adjustments and policy discussions that can leave many feeling overwhelmed. However, with the right knowledge and a proactive mindset, you can navigate these complexities and position yourself for optimal benefits. This comprehensive guide will delve into the critical strategies and considerations for anyone aiming to Maximize Social Security 2026, providing actionable insights to help you secure a more comfortable retirement.

Understanding the Fundamentals: How Social Security Works

Before we dive into maximization strategies, it’s essential to grasp the basics of how Social Security operates. Social Security is a pay-as-you-go system, meaning current workers’ contributions fund the benefits of today’s retirees and other beneficiaries. Your future benefits are primarily determined by your earnings history, specifically your highest 35 years of indexed earnings.

Your Primary Insurance Amount (PIA)

Your Primary Insurance Amount (PIA) is the benefit you receive if you claim at your Full Retirement Age (FRA). This age varies depending on your birth year. For those born in 1960 or later, your FRA is 67. The PIA is calculated using a progressive formula that gives a higher percentage of your past earnings to lower earners, but everyone benefits from higher lifetime earnings.

The Impact of Claiming Age

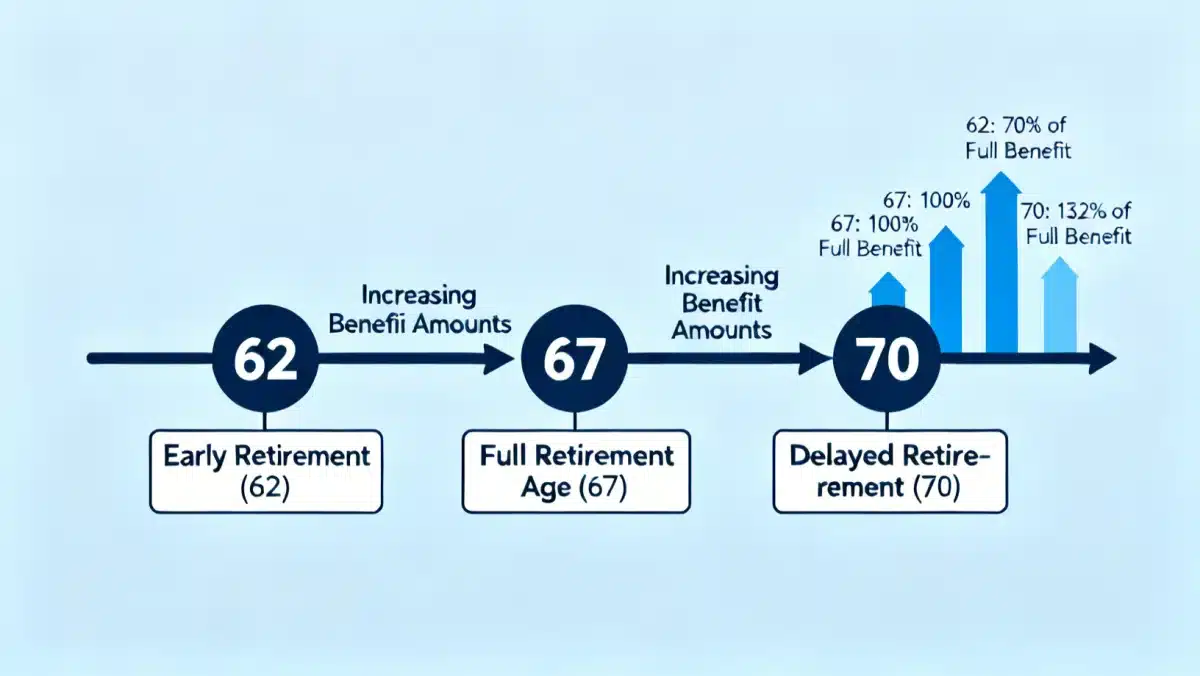

One of the most significant factors influencing your Social Security benefits is when you choose to claim them. You can claim as early as age 62, but doing so results in a permanent reduction in your monthly benefit. Conversely, delaying your claim past your FRA, up to age 70, can significantly increase your monthly payments due to delayed retirement credits. Understanding this trade-off is central to learning how to Maximize Social Security 2026.

Cost-of-Living Adjustments (COLA)

Each year, Social Security benefits are subject to a Cost-of-Living Adjustment (COLA) to help maintain the purchasing power of benefits in the face of inflation. While the 2026 COLA won’t be announced until late 2025, it’s a critical component of how your benefits will grow over time. Past COLAs have varied, and future adjustments will depend on economic indicators, particularly the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

Strategy 1: The Power of Delayed Claiming to Maximize Social Security 2026

The single most impactful strategy for increasing your monthly Social Security benefit is delaying when you start claiming it. While it might be tempting to claim at the earliest possible age (62), doing so can leave hundreds of dollars on the table each month for the rest of your life. For every year you delay claiming past your Full Retirement Age (FRA), up to age 70, your benefit increases by approximately 8% per year. This is a guaranteed, inflation-adjusted return on your decision, making it a powerful tool to Maximize Social Security 2026.

Understanding Your Full Retirement Age (FRA)

Your FRA depends on your birth year:

- Born 1943-1954: FRA is 66

- Born 1955: FRA is 66 and 2 months

- Born 1956: FRA is 66 and 4 months

- Born 1957: FRA is 66 and 6 months

- Born 1958: FRA is 66 and 8 months

- Born 1959: FRA is 66 and 10 months

- Born 1960 or later: FRA is 67

If your FRA is 67, and you delay claiming until age 70, you’ll accumulate 24% in delayed retirement credits (3 years x 8% per year). This means your monthly benefit at age 70 will be 124% of what it would have been at your FRA. This substantial increase can easily account for a significant portion of that extra $500 you’re aiming for.

The Break-Even Point

Many people worry about the “break-even point” – how long it takes for the higher delayed benefit to compensate for the years of foregone benefits. While this calculation is personal and depends on your life expectancy, for most individuals, delaying until age 70 pays off if they live into their late 70s or early 80s. Given increasing life expectancies, this strategy often makes strong financial sense, especially for those in good health. Don’t underestimate the long-term impact of this decision when planning to Maximize Social Security 2026.

Strategy 2: Navigating Spousal and Survivor Benefits

Social Security isn’t just for individual workers; it also provides crucial benefits for spouses and survivors. Understanding these rules can be a powerful way to Maximize Social Security 2026 for couples and families, potentially adding hundreds of dollars to household income.

Spousal Benefits

If you are married, divorced, or widowed, you may be eligible for spousal benefits based on your spouse’s (or ex-spouse’s) work record. A spouse can receive up to 50% of their partner’s Primary Insurance Amount (PIA) if they claim at their own Full Retirement Age. However, if they claim spousal benefits before their FRA, the amount will be reduced.

A key strategy for couples is to coordinate their claiming decisions. For example, one spouse with a lower earning history might claim spousal benefits while the higher-earning spouse delays their own claim to maximize their individual benefit (and thus, the potential survivor benefit). This can be a complex decision and often benefits from professional guidance to truly Maximize Social Security 2026 for your household.

- Claiming Spousal Benefits When Your Spouse Has Not Filed: This used to be a popular strategy (known as “file and suspend” or “restricted application”), but legislative changes in 2016 largely eliminated it for those born after January 1, 1954. If you were born on or before January 1, 1954, you might still be able to file a restricted application for spousal benefits at your FRA, allowing your own benefit to continue growing until age 70.

- Divorced Spousal Benefits: If you were married for at least 10 years, are currently unmarried, and are at least 62, you could be eligible for benefits based on your ex-spouse’s record. This won’t affect your ex-spouse’s benefits or those of their current spouse. This is often an overlooked opportunity to Maximize Social Security 2026.

Survivor Benefits

When a worker dies, their surviving spouse, children, or dependent parents may be eligible for survivor benefits. A surviving spouse can receive 100% of the deceased worker’s benefit if they claim at their FRA. If they claim earlier, the benefit is reduced. It’s crucial for surviving spouses to understand their options, as they may be able to claim one benefit (e.g., survivor benefit) while allowing their own earned benefit to grow, then switch to the higher benefit later.

For instance, a widow or widower at age 60 (or 50 if disabled) can claim survivor benefits. If their own earned benefit is higher, they could claim survivor benefits from age 60 until their own FRA, then switch to their own maximized benefit at age 70. This strategic claiming can significantly contribute to efforts to Maximize Social Security 2026 and beyond.

Strategy 3: Working Longer and Higher Earnings

Your Social Security benefits are calculated based on your 35 highest-earning years. If you have fewer than 35 years of work, or if some of your earlier years were low-earning years (perhaps due to part-time work, unemployment, or starting a career), continuing to work can increase your benefit. Each additional year of higher earnings can replace a lower-earning year in your top 35, thus increasing your overall average and your PIA.

Replacing Zero-Earning Years

If you have any years with zero earnings in your 35-year calculation, even a modest income in a later year can significantly boost your average. This is a straightforward yet often overlooked method to Maximize Social Security 2026.

The Earnings Test Before Full Retirement Age

If you claim Social Security benefits before your Full Retirement Age and continue to work, your benefits may be reduced if your earnings exceed certain limits. This is known as the “earnings test.”

- Before the year you reach FRA: For 2024, if you are under FRA for the entire year, Social Security deducts $1 from your benefits for every $2 you earn above an annual limit ($22,320 in 2024).

- In the year you reach FRA: Social Security deducts $1 from your benefits for every $3 you earn above a different, higher limit ($59,520 in 2024) until the month you reach your FRA. Once you reach your FRA, the earnings test no longer applies, and you can earn as much as you want without your benefits being reduced.

It’s important to note that any benefits withheld due to the earnings test are not lost forever. When you reach your FRA, your monthly benefit will be recalculated to account for the months benefits were withheld, potentially increasing your future payments. However, for immediate maximization, avoiding the earnings test by delaying claiming can be beneficial.

Strategy 4: Understanding and Leveraging COLAs for 2026 and Beyond

The Cost-of-Living Adjustment (COLA) is a critical, yet often misunderstood, aspect of Social Security. While you can’t directly influence the COLA, understanding how it works and its implications can help you better plan and appreciate how your benefits will grow over time, aiding your efforts to Maximize Social Security 2026‘s purchasing power.

How COLA is Calculated

COLA is determined by the increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the previous year to the third quarter of the current year. If there’s no increase, there’s no COLA. The Social Security Administration announces the COLA for the upcoming year each October. So, the 2026 COLA will be announced in October 2025.

The Impact of COLA on Delayed Benefits

An often-overlooked advantage of delaying your Social Security claim is that your future benefit continues to be adjusted by COLA even before you start receiving payments. This means that if you delay claiming from your FRA (e.g., 67) to age 70, not only do you get the 8% annual delayed retirement credits, but your base benefit also grows with each year’s COLA. This compounding effect can lead to a significantly higher monthly payment at age 70, further helping you Maximize Social Security 2026 and subsequent years.

For example, if your FRA is 67 and your PIA is $2,000, and there’s a 3% COLA each year, by age 70, your benefit would be:

- Age 67 PIA: $2,000

- Age 68 (after 3% COLA): $2,060

- Age 69 (after 3% COLA): $2,121.80

- Age 70 (after 3% COLA): $2,185.45

Then, apply the 24% delayed retirement credits to this COLA-adjusted amount: $2,185.45 * 1.24 = $2,710.96. This is a much higher benefit than if you had simply taken $2,000 at age 67 and applied COLA only to your payments. This compounding of COLA and delayed retirement credits is a powerful strategy to Maximize Social Security 2026 benefits.

Strategy 5: Factoring in Taxation of Social Security Benefits

It’s a common misconception that Social Security benefits are tax-free. For many retirees, a portion of their benefits can be subject to federal income tax, and in some states, even state income tax. Understanding these rules is crucial for financial planning and indirectly helps you Maximize Social Security 2026 by retaining more of your hard-earned benefits.

Federal Income Tax on Social Security

Whether your benefits are taxable depends on your “provisional income,” which is the sum of your adjusted gross income (AGI), tax-exempt interest (like from municipal bonds), and half of your Social Security benefits.

- Up to 50% of your benefits may be taxable if your provisional income is between $25,000 and $34,000 for an individual, or between $32,000 and $44,000 for a married couple filing jointly.

- Up to 85% of your benefits may be taxable if your provisional income is above $34,000 for an individual or above $44,000 for a married couple filing jointly.

There are no income thresholds below which 0% of your benefits are taxable.

Strategies to Minimize Taxation

- Manage Your Provisional Income: This is the most direct way to reduce the taxability of your Social Security. Consider strategies like Roth conversions in lower-income years (before claiming Social Security), strategic withdrawals from different types of retirement accounts (taxable, tax-deferred, tax-free), and carefully timing capital gains.

- Location Matters: Some states tax Social Security benefits, while others do not. If you’re considering a move in retirement, researching state tax laws could be beneficial. As of late 2023, 10 states tax Social Security benefits: Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Utah, Vermont, and West Virginia. However, many of these states offer exemptions for lower-income beneficiaries.

- Tax-Efficient Investing: Prioritize tax-advantaged accounts like Roth IRAs and HSAs for retirement savings, as withdrawals from these accounts are generally tax-free and do not count towards provisional income. This can be a long-term strategy to Maximize Social Security 2026‘s net value.

Strategy 6: Understanding the Role of Medicare Premiums

For most people, Medicare premiums are deducted directly from their Social Security checks. While this doesn’t directly affect the calculation of your Social Security benefit, it absolutely impacts the net amount you receive. Understanding how these premiums work, especially the Income-Related Monthly Adjustment Amount (IRMAA), is vital for comprehensive financial planning and effectively helps to Maximize Social Security 2026‘s take-home pay.

Standard Medicare Part B Premium

The standard Medicare Part B premium changes annually. For 2024, it was $174.70 per month. This amount is typically deducted from your Social Security benefit.

Income-Related Monthly Adjustment Amount (IRMAA)

If your Modified Adjusted Gross Income (MAGI) exceeds certain thresholds, you will pay a higher Medicare Part B and Part D premium. This is known as IRMAA. The Social Security Administration (SSA) uses your tax return from two years prior to determine your IRMAA. For example, your 2026 IRMAA will be based on your 2024 tax return.

IRMAA thresholds are typically adjusted annually. Exceeding these thresholds can add hundreds of dollars to your monthly Medicare premiums, significantly reducing your net Social Security income. This is a critical consideration for those looking to Maximize Social Security 2026‘s actual value.

Strategies to Manage IRMAA

- Manage Your MAGI: Similar to managing provisional income for Social Security taxation, managing your MAGI in the two years preceding your Medicare enrollment or an IRMAA determination year is key. This might involve strategic Roth conversions, tax-loss harvesting, or delaying large taxable withdrawals from retirement accounts.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older, you can make qualified charitable distributions directly from your IRA to a qualified charity. These distributions count towards your Required Minimum Distributions (RMDs) but are not included in your AGI, which can help lower your MAGI and potentially avoid IRMAA.

- Health Savings Accounts (HSAs): HSAs offer a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Using HSA funds for medical expenses (including Medicare premiums, though not IRMAA surcharges) can help preserve other taxable assets, thereby potentially lowering your MAGI.

Putting It All Together: A Holistic Approach to Maximize Social Security 2026

Achieving an extra $500 or more in monthly Social Security benefits by 2026 requires a holistic and integrated approach to your retirement planning. It’s rarely about one single decision but rather a combination of informed choices made over time.

1. Get Your Social Security Statement

The first step is always to understand where you stand. Create an account at ssa.gov/myaccount to access your personalized Social Security statement. This statement provides your earnings history and estimates your benefits at different claiming ages (62, FRA, and 70). This is your baseline for all planning to Maximize Social Security 2026.

2. Evaluate Your Health and Longevity

Your health and family longevity history are crucial factors. If you anticipate living a long life, delaying benefits until age 70 becomes a much more compelling strategy, as you’ll collect the higher payment for more years, significantly increasing your lifetime benefits. This is a key personal factor in deciding how to Maximize Social Security 2026.

3. Assess Your Other Retirement Income Sources

How much do you have in 401(k)s, IRAs, pensions, and other savings? Can these funds bridge the gap if you delay claiming Social Security? Understanding your complete financial picture helps you determine the feasibility of delaying benefits and managing provisional income for tax purposes. A robust retirement portfolio can provide the flexibility needed to Maximize Social Security 2026.

4. Coordinate with Your Spouse

If you’re married, discuss claiming strategies as a couple. Consider the higher earner delaying, spousal benefits, and survivor benefits. A coordinated strategy can yield significantly more for the household than individual, uncoordinated decisions. This is an area where couples can truly Maximize Social Security 2026 together.

5. Consider Professional Advice

Social Security rules can be complex, and every individual’s situation is unique. A qualified financial advisor specializing in retirement planning can help you analyze your specific circumstances, run various claiming scenarios, and develop a personalized strategy to Maximize Social Security 2026 and beyond. They can also help you integrate Social Security into your broader retirement and tax plan.

Preparing for 2026: What to Do Now

Even though 2026 is still a few years away, the time to plan is now. Here’s a checklist for immediate action:

- Review Your Earnings Record: Check your Social Security statement for accuracy. Any errors could negatively impact your benefits.

- Understand Your Full Retirement Age: Know precisely when you reach your FRA and how delaying past it affects your benefits.

- Estimate Your Benefits: Use the SSA’s online tools to estimate your benefits at different claiming ages.

- Model Different Scenarios: Consider how various claiming ages, work scenarios, and spousal coordination might impact your overall retirement income.

- Start a “Social Security Bridge” Fund: If you plan to delay claiming, consider setting aside funds to cover living expenses during the years you delay. This bridge fund can be crucial to making the delayed claiming strategy viable and helping you Maximize Social Security 2026.

- Educate Yourself on Tax Implications: Understand how your provisional income affects the taxation of benefits and Medicare premiums.

Conclusion: Your Path to Maximized Social Security Benefits

Maximizing your Social Security benefits in 2026, and potentially unlocking an extra $500 or more per month, is an achievable goal with careful planning and an understanding of the available strategies. From the profound impact of delayed claiming and the intricacies of spousal and survivor benefits to the importance of continuous earnings, COLA adjustments, and tax considerations, each piece plays a vital role in your overall retirement security.

Don’t leave hundreds of dollars on the table. Take control of your financial future by proactively engaging with your Social Security options. By applying these insider strategies, you can confidently navigate the system and ensure you are positioned to Maximize Social Security 2026 for a more prosperous and secure retirement.

and IRA Limits")