Maximize 2026 IRA Contributions: Boost Retirement Savings by 15%

In the intricate landscape of personal finance, securing your retirement is often hailed as one of the most critical objectives. As we look towards 2026, the opportunity to significantly enhance your retirement nest egg through strategic IRA contributions becomes increasingly apparent. This comprehensive guide is designed to empower you with the knowledge and actionable strategies to not only maximize IRA contributions but also potentially boost your retirement savings by an impressive 15%. We’ll delve into the nuances of various IRA types, explore advanced contribution tactics, and provide practical solutions to ensure your financial future is as robust as possible.

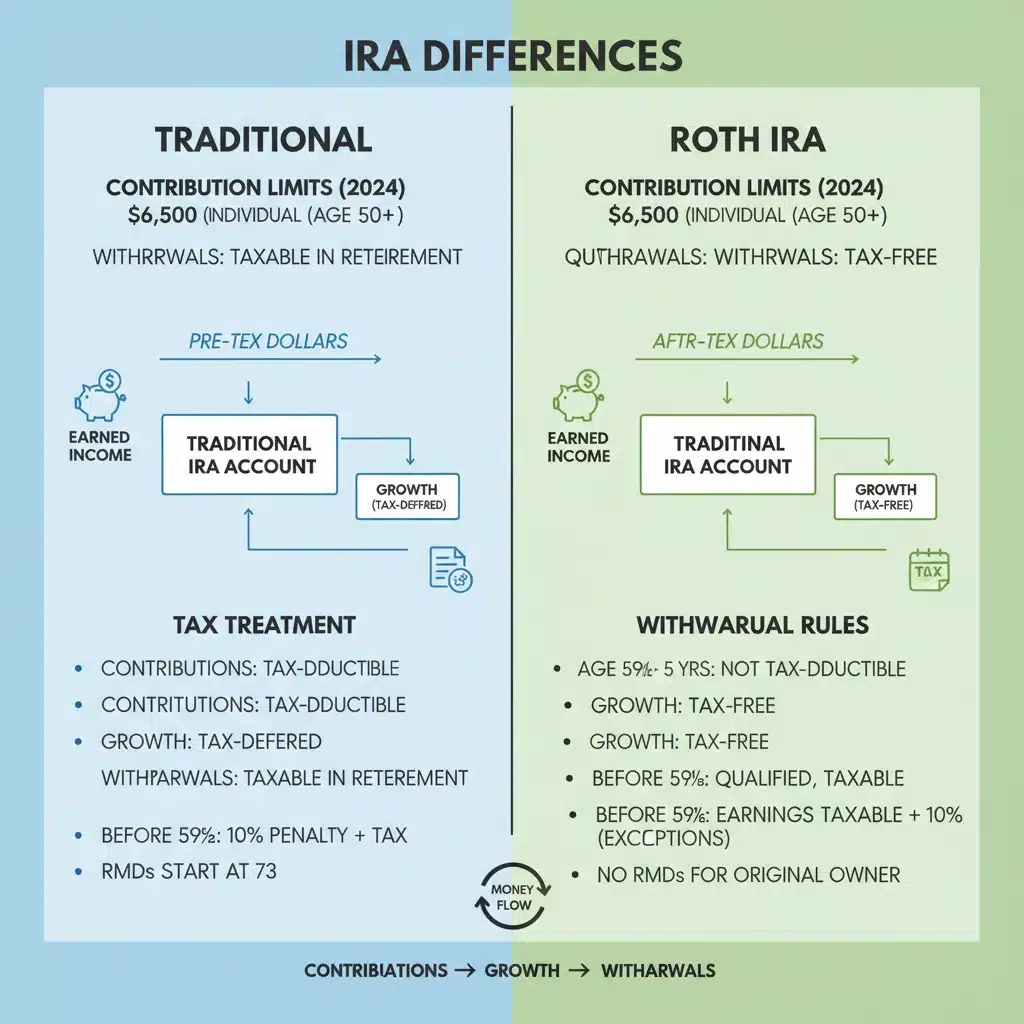

Understanding the Foundation: Traditional vs. Roth IRAs

Before we can effectively maximize IRA contributions, it’s crucial to understand the fundamental differences between the two primary types of Individual Retirement Arrangements: Traditional IRAs and Roth IRAs. Each offers distinct tax advantages and withdrawal rules, making the choice highly dependent on your current financial situation, income level, and future tax expectations.

Traditional IRA: Immediate Tax Benefits

A Traditional IRA allows pre-tax contributions to grow tax-deferred. This means you don’t pay taxes on the money until retirement, and in many cases, your contributions are tax-deductible in the year they are made. The immediate tax deduction can significantly lower your taxable income in the present, which is particularly appealing for individuals who expect to be in a lower tax bracket during retirement than they are currently. However, withdrawals in retirement are taxed as ordinary income. The deductibility of your Traditional IRA contributions can be limited if you or your spouse are covered by a retirement plan at work and your income exceeds certain thresholds.

Roth IRA: Tax-Free Growth and Withdrawals

Conversely, a Roth IRA is funded with after-tax dollars. While there’s no upfront tax deduction for contributions, the magic of a Roth IRA lies in its tax-free growth and, most importantly, tax-free qualified withdrawals in retirement. This makes it an incredibly powerful tool if you anticipate being in a higher tax bracket during retirement than you are now. Roth IRAs also offer more flexibility, as contributions can be withdrawn tax- and penalty-free at any time, for any reason, though earnings typically require you to be at least 59½ years old and have had the account open for five years. However, there are income limitations for directly contributing to a Roth IRA, which we will explore later.

Contribution Limits for 2026

While the exact contribution limits for 2026 are subject to inflation adjustments, we can project them based on current trends. For 2025, the IRA contribution limit for those under age 50 is $7,000, and for those age 50 and over, it’s $8,000 (including the $1,000 catch-up contribution). It’s reasonable to anticipate a slight increase for 2026, perhaps to $7,500 and $8,500 respectively. Staying informed about these official figures as they are released by the IRS will be your first step to maximize IRA contributions for the year.

Strategic Approaches to Maximize IRA Contributions

Beyond simply contributing the maximum allowable amount, several strategic approaches can help you significantly boost your retirement savings. These strategies often involve understanding income phase-outs, leveraging spousal IRAs, and even utilizing advanced techniques like the ‘backdoor Roth’.

1. Max Out Your Contributions Annually

This might seem obvious, but consistently contributing the maximum allowed amount each year is the most direct way to maximize IRA contributions. Many individuals contribute less than the maximum, missing out on years of tax-advantaged growth. Even if you can’t contribute the full amount at the beginning of the year, setting up automated monthly contributions can help you reach the limit by tax day.

2. Don’t Forget Catch-Up Contributions

If you’re age 50 or older, the IRS allows you to make additional ‘catch-up’ contributions to your IRA. As mentioned, for 2025, this is an additional $1,000. This provision is incredibly valuable for those who started saving later in life or who want to accelerate their retirement savings in their prime earning years. Make sure to factor this into your 2026 planning to truly maximize IRA contributions.

3. The Power of a Spousal IRA

If you’re married and file jointly, and one spouse earns little or no income, a spousal IRA allows the non-working or lower-earning spouse to contribute to an IRA based on the working spouse’s income. This effectively doubles the amount your household can contribute to IRAs each year, significantly accelerating your combined retirement savings. Both spouses can contribute up to the individual maximum, plus any applicable catch-up contributions, to their respective IRAs.

4. The Backdoor Roth IRA Strategy

For high-income earners whose Modified Adjusted Gross Income (MAGI) exceeds the limits for direct Roth IRA contributions, the ‘backdoor Roth’ strategy provides a legal and effective way to contribute to a Roth IRA. This involves making a non-deductible contribution to a Traditional IRA and then immediately converting those funds to a Roth IRA. While the conversion itself is a taxable event if you have any pre-tax IRA money (due to the pro-rata rule), if it’s a ‘clean’ non-deductible contribution, it can be converted tax-free. This is a powerful tactic to maximize IRA contributions for those otherwise locked out of direct Roth contributions. It’s crucial to consult with a financial advisor to ensure this strategy is executed correctly and to understand its tax implications, especially regarding the pro-rata rule if you have existing pre-tax IRA accounts.

Advanced Strategies to Boost Your Savings by 15%

Achieving a 15% boost in your retirement savings isn’t just about maximizing contributions; it’s also about optimizing your investment strategy, minimizing fees, and leveraging compounding interest effectively. Here’s how to take your efforts to maximize IRA contributions to the next level.

1. Optimize Your Investment Portfolio Within Your IRA

Simply contributing to an IRA isn’t enough; the funds need to be invested wisely. A well-diversified portfolio tailored to your risk tolerance and time horizon can significantly enhance returns. Consider low-cost index funds, exchange-traded funds (ETFs), or target-date funds. Over the long term, even a small increase in your annual return can lead to substantial growth. For example, if you consistently earn an additional 1-2% return on your investments, compounded over decades, this can easily translate to a 15% or more boost in your final retirement sum.

2. Automate Your Contributions

One of the simplest yet most effective ways to ensure you maximize IRA contributions is to automate them. Set up recurring transfers from your checking account to your IRA every pay period. This ‘set it and forget it’ approach helps you stay disciplined, avoids the temptation to spend the money elsewhere, and ensures you consistently contribute throughout the year, taking advantage of dollar-cost averaging.

3. Leverage Tax Refunds for Lump-Sum Contributions

If you typically receive a tax refund, consider directing a portion or all of it directly into your IRA. This lump-sum contribution can provide a significant boost to your annual total, especially if you’re struggling to reach the maximum through regular contributions. It’s found money that can be put to excellent use in your retirement plan.

4. Rebalance Your Portfolio Regularly

Over time, your portfolio’s original asset allocation can drift due to market performance. Regularly rebalancing (e.g., annually) helps you maintain your desired risk level and ensures you’re not overexposed to certain assets. This disciplined approach can help protect gains and keep your investments aligned with your long-term goals, contributing to that 15% boost.

5. Be Mindful of Fees

High investment fees, even seemingly small ones, can erode a significant portion of your returns over decades. When choosing funds or investment platforms for your IRA, pay close attention to expense ratios, trading fees, and account maintenance fees. Opt for low-cost options to ensure more of your money is working for you, not for the financial institution. This subtle but powerful strategy directly impacts your ability to maximize IRA contributions‘ growth potential.

The Role of Compounding Interest in Boosting Your Savings

The concept of compounding interest is often called the ‘eighth wonder of the world’ for a good reason. It’s the process where your investments earn returns, and those returns then earn their own returns. The earlier you start to maximize IRA contributions, the more time compounding has to work its magic.

Consider this hypothetical: If you contribute $7,000 annually to an IRA earning an average of 7% per year, after 30 years, you would have contributed $210,000, but your account balance could be over $700,000. If you were able to increase your contribution by just 15% (an additional $1,050 per year, totaling $8,050 annually), your final balance could be significantly higher, demonstrating the profound impact of maximizing contributions and leveraging compounding over the long term.

Navigating Income Limitations for Roth IRAs

While the benefits of a Roth IRA are substantial, direct contributions are subject to income limitations. For 2025, if your Modified Adjusted Gross Income (MAGI) is between $146,000 and $161,000 for single filers, or between $230,000 and $240,000 for those married filing jointly, your ability to contribute directly to a Roth IRA is phased out. Above these upper limits, you cannot contribute directly. This is where the backdoor Roth IRA strategy becomes indispensable for high-income earners who still wish to benefit from tax-free growth and withdrawals, allowing them to effectively maximize IRA contributions despite income restrictions.

Pro-Rata Rule Considerations for Backdoor Roth

A critical aspect of the backdoor Roth strategy is understanding the ‘pro-rata’ rule. If you have existing pre-tax money in any Traditional, SEP, or SIMPLE IRA accounts, a portion of your Roth conversion will be taxable. The IRS views all your non-Roth IRA accounts as one for tax purposes. Therefore, if you convert a non-deductible Traditional IRA contribution to a Roth, but also have other pre-tax IRA money, the conversion will be proportionally taxed. To avoid this, some individuals consider rolling over pre-tax IRA funds into a 401(k) or similar employer-sponsored plan before executing a backdoor Roth conversion, if their plan allows it. This is a complex area, and professional tax advice is highly recommended to ensure compliance and avoid unexpected tax liabilities when you maximize IRA contributions through this method.

The Importance of Regular Review and Adjustment

Financial planning is not a one-time event; it’s an ongoing process. To consistently maximize IRA contributions and ensure your retirement savings are on track, it’s essential to regularly review your financial situation and make adjustments as needed. This includes:

- Annual Review of Contribution Limits: Stay updated on the latest IRA contribution limits for 2026 and beyond, including catch-up contributions.

- Income Changes: If your income increases, you might be able to contribute more or need to consider strategies like the backdoor Roth IRA. If your income decreases, you might qualify for tax deductions you previously couldn’t claim.

- Life Events: Marriage, divorce, having children, or career changes can all impact your financial goals and your ability to save. Adjust your IRA contributions and overall financial plan accordingly.

- Investment Performance: Periodically assess the performance of your IRA investments. Are they meeting your expectations? Is your risk tolerance still aligned with your portfolio?

- Tax Law Changes: Tax laws can change, potentially impacting the attractiveness of Traditional vs. Roth IRAs or the mechanics of strategies like the backdoor Roth. Stay informed or work with a financial professional.

Putting It All Together: A 15% Boost in Retirement Savings

Achieving a 15% boost in your retirement savings through your IRA contributions in 2026 is an ambitious yet entirely attainable goal. It requires a combination of disciplined saving, strategic planning, and continuous optimization. Here’s a summary of how these strategies can collectively lead to such a significant enhancement:

- Maximize Annual Contributions: Consistently contributing the maximum allowable amount, including catch-up contributions if eligible, forms the bedrock of this boost. If the 2026 limit is $7,500 (under 50), ensuring you hit this target is paramount.

- Leverage Spousal IRAs: For married couples, effectively doubling your IRA contributions through a spousal IRA can provide a substantial leap in overall savings.

- Strategic Use of Backdoor Roth: High-income earners can bypass direct Roth contribution limits, ensuring their post-tax savings grow tax-free, adding a powerful layer to their retirement wealth.

- Optimized Investment Strategy: Investing your IRA funds in a diversified, low-cost portfolio that aligns with your risk tolerance can significantly enhance returns. A conservative estimate of a 1-2% higher annual return over decades can easily translate to a 15% cumulative increase in your final balance.

- Minimizing Fees: Every dollar saved on fees is a dollar that remains invested and compounds, directly contributing to your savings growth.

- Automated & Lump-Sum Contributions: Consistent, automated contributions combined with strategic lump-sum additions (like tax refunds) ensure you hit your targets without fail.

Imagine if, through these combined efforts, you increase your annual contribution by even a modest amount (e.g., an extra $500-$1,000) and simultaneously enhance your investment returns by 1%. Over 20-30 years, the compounded effect of these actions can easily lead to a retirement fund that is 15% larger than it would have been with a more passive approach. This percentage isn’t just a number; it represents increased financial freedom, greater security, and potentially an earlier or more comfortable retirement.

Conclusion: Take Control of Your Retirement Future

The journey to a secure and prosperous retirement is a marathon, not a sprint. By focusing on how to maximize IRA contributions in 2026 and implementing the advanced strategies outlined in this guide, you are not just saving; you are actively building a more robust financial future. Whether you lean towards the immediate tax benefits of a Traditional IRA or the long-term tax-free growth of a Roth, the key is to be proactive, informed, and strategic. Don’t let another year pass without fully leveraging the power of your IRA. Start planning today, consult with a qualified financial advisor to tailor these strategies to your unique situation, and take confident steps towards achieving that significant 15% boost in your retirement savings.

Your future self will thank you for the diligence and foresight you apply to your IRA contributions now.

Contribution Limits 2026: Maximize Your Retirement Savings")

and IRA Limits")

Limits & Roth IRA Benefits")