Federal Student Loan Forgiveness 2026: Updates, Eligibility & Repayment Plans

Student loan debt continues to be a significant financial burden for millions of Americans. As we look ahead to 2026, understanding the landscape of federal student loan forgiveness programs and repayment options is more crucial than ever. The policies and programs surrounding student debt are constantly evolving, making it essential for borrowers to stay informed about the latest updates, eligibility criteria, and how these changes might impact their financial future. This comprehensive guide will delve into the anticipated developments for student loan forgiveness 2026, offering a clear roadmap through the complexities of federal student aid.

The journey to deciphering student loan forgiveness can often feel overwhelming, with acronyms and nuanced rules creating a maze for borrowers. However, with careful consideration and strategic planning, it is possible to navigate these waters successfully. Our aim is to demystify the process, providing you with actionable insights and a thorough comparison of the most relevant repayment plans, including the much-discussed SAVE Plan, PAYE, and ICR. Whether you are actively seeking forgiveness, exploring options to lower your monthly payments, or simply trying to understand the future of your student debt, this article is designed to be your go-to resource.

The Evolving Landscape of Federal Student Loan Forgiveness

The past few years have seen unprecedented changes in federal student loan policies. From pandemic-related payment pauses to significant shifts in income-driven repayment (IDR) plans and targeted forgiveness initiatives, borrowers have had to adapt quickly. As we approach 2026, it’s important to recognize that while some programs are well-established, others are still being refined or are subject to potential legislative changes. Staying abreast of these developments is key to maximizing your chances of achieving student loan forgiveness 2026.

The Department of Education and various administrations have shown a commitment to addressing the student debt crisis, albeit through different approaches. This has led to a dynamic environment where eligibility requirements and program benefits can shift. It’s not enough to simply know about a forgiveness program; understanding its specific conditions, the types of loans it applies to, and the necessary steps for application is paramount. We’ll explore the main avenues for federal student loan forgiveness and what borrowers can expect in the coming years.

Key Forgiveness Programs to Watch for in 2026

Several federal student loan forgiveness programs are likely to remain central to discussions and borrower strategies in 2026. These include:

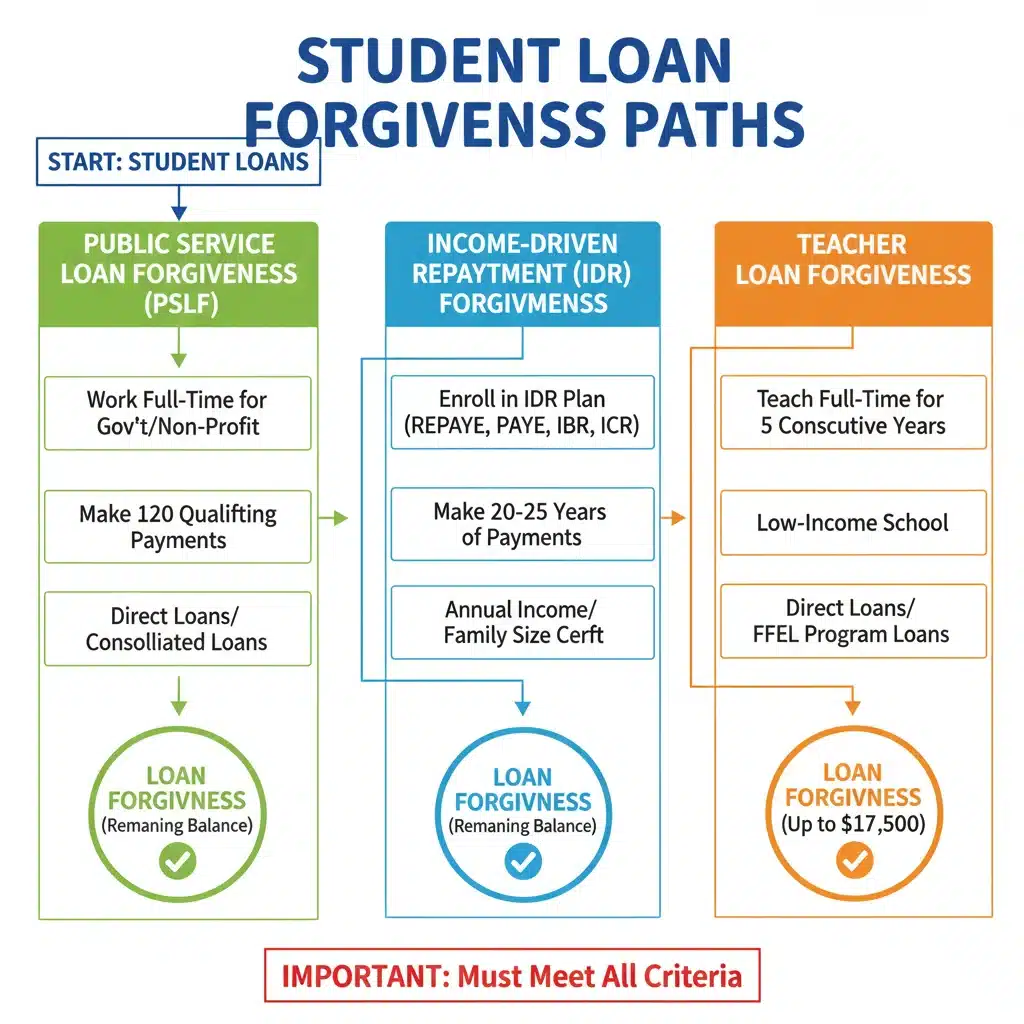

- Public Service Loan Forgiveness (PSLF): This program is designed for individuals working in qualifying public service jobs. After 120 qualifying monthly payments, borrowers may have the remainder of their Direct Loan balance forgiven. Understanding what constitutes a ‘qualifying’ employer and ‘qualifying’ payments is critical.

- Income-Driven Repayment (IDR) Forgiveness: Under IDR plans, any remaining loan balance is forgiven after 20 or 25 years of payments, depending on the plan and whether the loans are for undergraduate or graduate study. Recent adjustments to IDR account adjustments have brought many borrowers closer to forgiveness.

- Teacher Loan Forgiveness (TLF): Specific to teachers working in low-income schools or educational service agencies, this program offers up to $17,500 in forgiveness for Direct Subsidized and Unsubsidized Loans, and Federal Stafford Loans, after five complete and consecutive years of teaching.

- Total and Permanent Disability (TPD) Discharge: Borrowers who are permanently disabled may qualify to have their federal student loans discharged. This often requires documentation from a physician, the Social Security Administration, or the Department of Veterans Affairs.

- Borrower Defense to Repayment: This mechanism allows borrowers to seek forgiveness if their school misled them or engaged in other misconduct in violation of certain state laws.

- Closed School Discharge: If your school closed while you were enrolled or shortly after you withdrew, you might be eligible for a discharge of your federal student loans.

Each of these programs has distinct eligibility criteria and application processes. For borrowers aiming for student loan forgiveness 2026, it’s vital to identify which program aligns best with their circumstances and to meticulously track their progress and documentation.

Eligibility Criteria for Student Loan Forgiveness in 2026

Navigating the eligibility requirements for federal student loan forgiveness programs can be complex, as each program has its own set of rules. However, there are some overarching principles and specific criteria that borrowers should be aware of to determine their potential for student loan forgiveness 2026.

General Eligibility Considerations

Most federal student loan forgiveness programs generally require:

- Federal Loans: The loans must be federal student loans. Private student loans are typically not eligible for federal forgiveness programs. Direct Loans are usually the most eligible, while FFEL Program loans and Perkins Loans may require consolidation into a Direct Consolidation Loan to qualify for certain programs, especially PSLF and some IDR benefits.

- On-Time Payments (or Qualifying Periods): Forgiveness often hinges on making a specified number of qualifying payments or serving in a particular capacity for a set period. The definition of a ‘qualifying payment’ can vary by program.

- Specific Employment/Circumstances: Many programs, like PSLF or Teacher Loan Forgiveness, are tied to specific types of employment. TPD discharge is tied to a medical condition, and Borrower Defense to Repayment is tied to school misconduct.

- Application Process: Borrowers must typically apply for forgiveness, and the application process can involve submitting extensive documentation.

Deep Dive into PSLF Eligibility for 2026

The Public Service Loan Forgiveness (PSLF) program continues to be a cornerstone for many public servants. For student loan forgiveness 2026 under PSLF, key eligibility factors include:

- Loan Type: Only Direct Loans qualify. If you have FFEL or Perkins Loans, you’ll need to consolidate them into a Direct Consolidation Loan.

- Employment: You must be employed full-time by a U.S. federal, state, local, or tribal government organization (this includes the military) or a not-for-profit organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code. Other not-for-profit organizations that provide certain public services may also qualify.

- Repayment Plan: You must make 120 qualifying monthly payments while on an income-driven repayment (IDR) plan or the 10-year Standard Repayment Plan. Payments made under other plans (like the Extended or Graduated Plans) do not count towards PSLF unless they were made during the temporary waiver periods.

- Payment Requirements: Payments must be made on time, for the full amount due, and after October 1, 2007.

It’s crucial for PSLF-seeking borrowers to submit the PSLF Form (Employment Certification Form) annually or whenever they change employers. This helps track qualifying employment and payments, preventing issues down the line when applying for student loan forgiveness 2026.

Understanding and Comparing Repayment Plans for Forgiveness

Choosing the right repayment plan is paramount, especially when aiming for student loan forgiveness 2026. Many forgiveness programs, particularly PSLF and IDR forgiveness, are directly tied to enrollment in specific repayment plans. Understanding the nuances of each plan can significantly impact your monthly payments, the total amount you pay over time, and your eligibility for ultimate forgiveness.

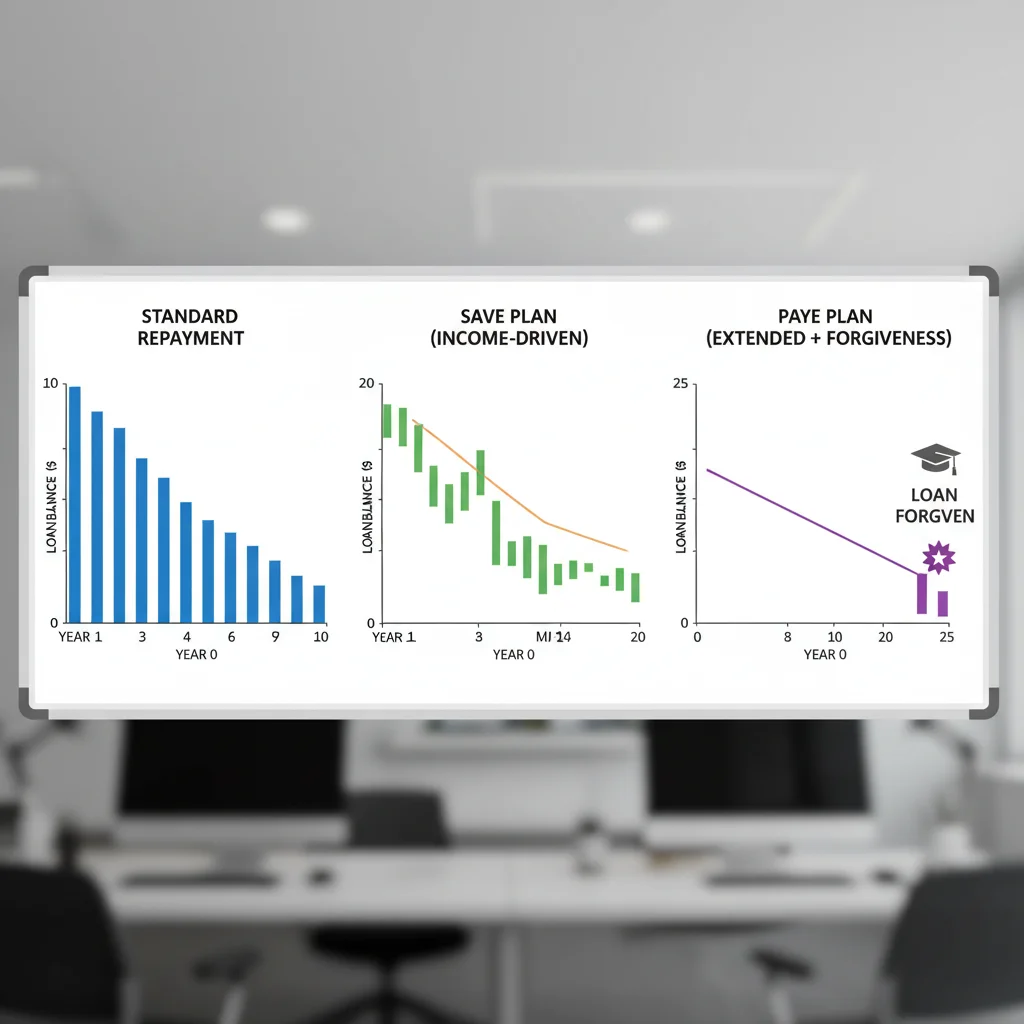

The Standard Repayment Plan

The Standard Repayment Plan is the default plan for most federal student loans. Under this plan, you pay a fixed amount each month for up to 10 years (or up to 30 years for Direct Consolidation Loans and FFEL Consolidation Loans). While it typically results in paying the least amount of interest over the life of the loan and ensures your loans are paid off relatively quickly, it’s generally not the best path for most forgiveness programs, with the exception of PSLF where payments under this plan do count. However, the 10-year timeline often means there’s no balance left to forgive by the time PSLF eligibility is met.

Income-Driven Repayment (IDR) Plans: A Pathway to Forgiveness

Income-Driven Repayment (IDR) plans are designed to make student loan payments more affordable by capping them at a percentage of your discretionary income. These plans are crucial for borrowers seeking student loan forgiveness 2026, especially through IDR forgiveness or PSLF, as they allow for lower monthly payments that can count towards the required payment totals.

1. The SAVE Plan (Saving on a Valuable Education)

The SAVE Plan is the newest IDR plan and is replacing the REPAYE Plan. It’s designed to be the most affordable IDR plan, especially for low- and middle-income borrowers. Key features include:

- Payment Calculation: For undergraduate loans, payments are capped at 5% of discretionary income (down from 10% on REPAYE). For graduate loans, it’s 10%, and for a mix, it’s a weighted average.

- Interest Subsidy: A significant benefit is that if your calculated monthly payment doesn’t cover the monthly interest, the government covers the remaining interest, preventing your loan balance from growing due to unpaid interest. This is a game-changer for many borrowers.

- Lower Discretionary Income Definition: The SAVE Plan increases the amount of income protected from payment calculations to 225% of the federal poverty line, up from 150% on other IDR plans. This means more income is considered non-discretionary, leading to lower monthly payments for many.

- Forgiveness Timeline: Forgiveness is typically granted after 20 or 25 years of payments. However, a new provision allows for forgiveness as early as 10 years for borrowers with original principal balances of $12,000 or less, with an additional year added for every $1,000 borrowed above that amount, up to the standard 20 or 25 years.

- Spousal Income: Unlike PAYE and IBR, if you’re married and file taxes separately, your spouse’s income is not included in the payment calculation, which can be beneficial for some.

The SAVE Plan is poised to be a primary vehicle for student loan forgiveness 2026 for many borrowers, especially those with lower incomes and smaller loan balances.

2. Pay As You Earn (PAYE) Repayment Plan

The PAYE Plan is another popular IDR option, particularly for newer borrowers. Its features include:

- Payment Cap: Payments are generally 10% of your discretionary income, but they will never exceed what you would pay under the 10-year Standard Repayment Plan. This cap can be a significant advantage for borrowers whose income increases substantially over time.

- Forgiveness Timeline: Any remaining balance is forgiven after 20 years of qualifying payments.

- Eligibility: Only available to new borrowers on or after October 1, 2007, who also received a new loan on or after October 1, 2011.

- Spousal Income: If you’re married and file separately, your spouse’s income is generally excluded from the calculation.

3. Income-Contingent Repayment (ICR) Plan

The ICR Plan is the oldest IDR plan and is often considered a fallback for borrowers who don’t qualify for other IDR plans or who have Parent PLUS Loans consolidated into a Direct Consolidation Loan. Key aspects include:

- Payment Calculation: Payments are the lesser of 20% of your discretionary income or what you would pay on a fixed 12-year repayment plan, adjusted according to your income.

- Forgiveness Timeline: Any remaining balance is forgiven after 25 years of qualifying payments.

- Discretionary Income Definition: Discretionary income is defined as the difference between your adjusted gross income (AGI) and 100% of the federal poverty line.

- Spousal Income: If you’re married, your spouse’s income is included regardless of your tax filing status.

While often less generous than SAVE or PAYE, ICR remains an option for certain borrowers, particularly those with consolidated Parent PLUS loans seeking student loan forgiveness 2026.

Strategic Planning for Student Loan Forgiveness in 2026

Effective management of your student loans, with an eye toward student loan forgiveness 2026, requires proactive planning and a clear understanding of your individual circumstances. Here are strategic steps to consider:

1. Understand Your Loan Types

Not all student loans are created equal when it comes to forgiveness. Federal Direct Loans offer the most pathways to forgiveness. If you have FFEL Program loans or Perkins Loans, consider consolidating them into a Direct Consolidation Loan. This step is often necessary to qualify for PSLF and some IDR plans, and to benefit from the IDR account adjustments. Private student loans are almost never eligible for federal forgiveness programs.

2. Choose the Right Repayment Plan

As discussed, your choice of repayment plan is critical. If your goal is PSLF, you must be on an IDR plan or the 10-year Standard Repayment Plan. For IDR forgiveness, you need to be on one of the IDR plans (SAVE, PAYE, IBR, ICR). Use the Loan Simulator tool on StudentAid.gov to compare plans based on your income, family size, and loan balance. This tool can help you project monthly payments and potential forgiveness amounts, aiding your strategy for student loan forgiveness 2026.

3. Certify Your Employment (for PSLF)

If you are pursuing PSLF, submit the PSLF Form (Employment Certification Form) annually or whenever you change employers. This form verifies your qualifying employment and ensures your payments are being counted correctly. Don’t wait until you’ve made 120 payments to do this; regular certification helps catch and correct errors early.

4. Recertify Your Income Annually (for IDR Plans)

For all IDR plans, you must recertify your income and family size annually. Failing to do so can result in your payments increasing significantly or capitalized interest being added to your principal balance, which can undermine your efforts towards student loan forgiveness 2026. You will receive notifications from your loan servicer when it’s time to recertify.

5. Keep Accurate Records

Maintain meticulous records of all your student loan documents, including loan statements, payment confirmations, employment verification forms, and any correspondence with your loan servicer or the Department of Education. This documentation can be invaluable if there are discrepancies or issues when you apply for forgiveness.

6. Stay Informed About Policy Changes

Federal student loan policies are subject to change. Keep up-to-date with announcements from the Department of Education, especially regarding IDR account adjustments, potential new forgiveness initiatives, or modifications to existing programs. Reliable sources include StudentAid.gov and reputable financial news outlets. Changes made today could significantly impact your path to student loan forgiveness 2026.

7. Consider Consolidation Carefully

While consolidation can be beneficial for certain loan types (e.g., FFEL, Perkins) to qualify for IDR or PSLF, it can also restart your payment count for forgiveness programs if not done correctly or at the right time. Understand the implications of consolidation before proceeding. The IDR account adjustments have made consolidation more favorable for many, allowing past payments on consolidated loans to count, but always verify your specific situation.

8. Seek Professional Advice if Needed

If your situation is particularly complex, or you’re unsure about the best path forward, consider consulting with a non-profit student loan counselor or a financial advisor specializing in student debt. They can provide personalized guidance tailored to your financial situation and goals for student loan forgiveness 2026.

The Impact of the IDR Account Adjustment on Forgiveness

A significant development that continues to impact borrowers aiming for student loan forgiveness 2026 is the Income-Driven Repayment (IDR) account adjustment. This one-time adjustment by the Department of Education aims to correct past administrative failures and ensure borrowers receive appropriate credit toward IDR and PSLF forgiveness.

What the Adjustment Does:

- Counts More Payments: The adjustment credits borrowers with more months toward IDR and PSLF forgiveness, including periods of deferment (except in-school deferment), forbearance (for 12 consecutive months or more, or 36 cumulative months or more), and certain periods of repayment before 2013 that might not have been previously counted.

- Addresses Forbearance Steering: It specifically addresses concerns where servicers may have pushed borrowers into forbearance instead of IDR plans, which would have put them closer to forgiveness.

- Consolidation Benefits: For borrowers with older FFEL or Perkins loans, consolidating them into a Direct Consolidation Loan before a certain deadline (currently April 30, 2024, but always check for updates) allows the consolidated loan to receive credit for the oldest loan’s payment history, potentially accelerating forgiveness.

- Automatic Forgiveness: Many borrowers who reached the 20 or 25 years of payments (or 10 years for PSLF) after the adjustment have already received automatic forgiveness, totaling billions of dollars in debt relief.

This adjustment is a critical factor for anyone assessing their eligibility for student loan forgiveness 2026. Borrowers should check their loan status and payment counts on StudentAid.gov to see how this adjustment has affected their progress. If you believe you qualify for additional adjustments or need to consolidate to take advantage, act promptly.

Potential Future Changes and What They Mean for 2026

While we can analyze current programs and trends, the future of federal student loan policy is always subject to change. New legislative proposals, administrative actions, and even court challenges could introduce new programs or modify existing ones that impact student loan forgiveness 2026 and beyond.

Key Areas to Monitor:

- Legislative Action: Congress could introduce new laws to expand or restrict forgiveness programs, or to fundamentally reform the student loan system.

- Executive Actions: The executive branch might implement new policies or make further adjustments to existing programs, similar to the IDR account adjustment or the creation of the SAVE Plan.

- Economic Conditions: Broader economic conditions, such as inflation or recession, could influence policy decisions related to student debt relief.

- Court Challenges: Legal challenges to student loan policies have occurred in the past and could arise again, potentially impacting the implementation of certain programs.

Given this dynamic environment, borrowers should cultivate a habit of regularly checking official government sources, such as StudentAid.gov, for the most up-to-date and accurate information. Relying on unofficial sources or outdated information can lead to missed opportunities or incorrect assumptions about your eligibility for student loan forgiveness 2026.

Conclusion: Your Path to Student Loan Forgiveness in 2026

The journey toward federal student loan forgiveness in 2026 is multifaceted, requiring diligence, understanding, and proactive engagement. From identifying the correct loan types to choosing the optimal repayment plan and meticulously tracking your progress, each step is crucial. The introduction of the SAVE Plan and the ongoing IDR account adjustments represent significant opportunities for many borrowers to achieve relief sooner than anticipated.

By staying informed about the latest program updates, thoroughly understanding eligibility criteria, and strategically selecting the repayment plan that aligns with your financial goals and career path, you can significantly improve your chances of securing student loan forgiveness 2026. Remember to utilize official resources, maintain impeccable records, and seek expert advice when necessary. Your financial future is worth the effort, and with the right approach, managing your student loan debt and working towards forgiveness can become a clear and achievable goal.

Don’t let the complexity deter you. Break down the process into manageable steps, review your options regularly, and take advantage of every opportunity available to you. The landscape of student loan forgiveness is designed to offer pathways to relief, and with careful planning, 2026 could be the year you see substantial progress towards a debt-free future.